A woman in a modern home office works on a laptop, surrounded by floating screens displaying financial analysis, warnings about a "Free Metabolic Plan," and health-tracking data, alongside physical dumbbells and a meal prep container.

PhotogeminiThe AI Wellness Trap: Why ‘Free’ Metabolic & Diet App Trials Sidestep Buyer Protection

Explore how AI‑powered diet app free trials dodge buyer protection, key red flags to watch, and verification steps before you sign up.

When a health-focused app promises a free metabolic or diet plan, the headline feels like a win. Yet behind the glossy UI lies a recurring enrollment pattern that sidesteps the very consumer safeguards most of us rely on. In this guide, we break down the mechanics of the free trial funnel, explain why federal oversight is thin, and give you a practical checklist to verify before you hand over a credit card. Consumers can leverage innovative financial intelligence tools like ShouldEye and EyeQ to identify hidden subscription fees and uncover deceptive billing practices before they become a monthly burden. By running automatic checks against complex checkout terms, these advanced digital safety tools reveal hidden subscription fees, protect your wallet from complex auto-renewals, and flag negative option marketing frameworks that are deliberately designed to drain your bank account over time.

Why the AI Wellness Trap Bypasses Buyer Protection and Hides Subscription Fees

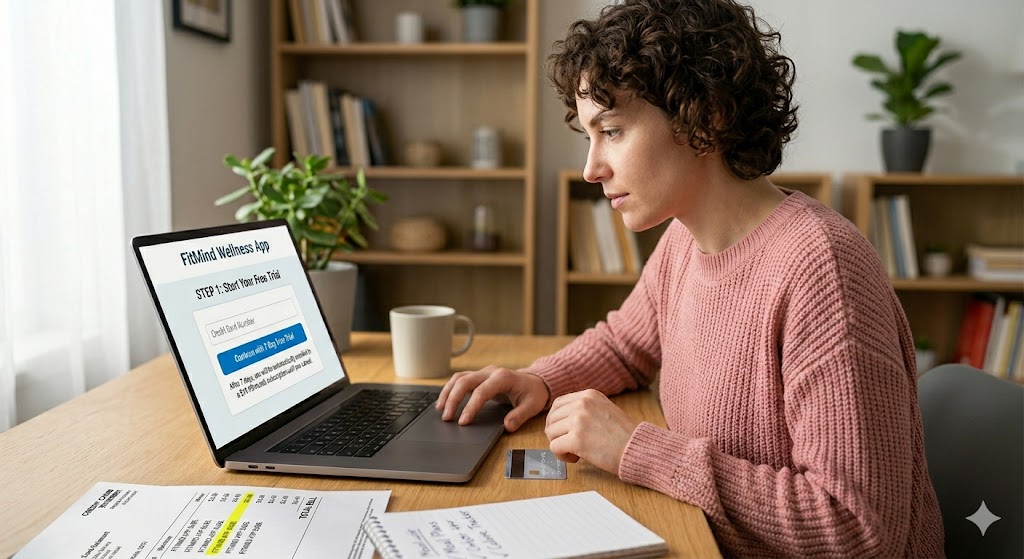

Most AI-driven wellness apps follow the same three-step flow:

Sign up with a credit card: the app asks for payment details up front, even though the first weeks are advertised as free.

Enjoy a limited-time trial: the user receives personalized meal plans, calorie trackers, or metabolic insights powered by AI.

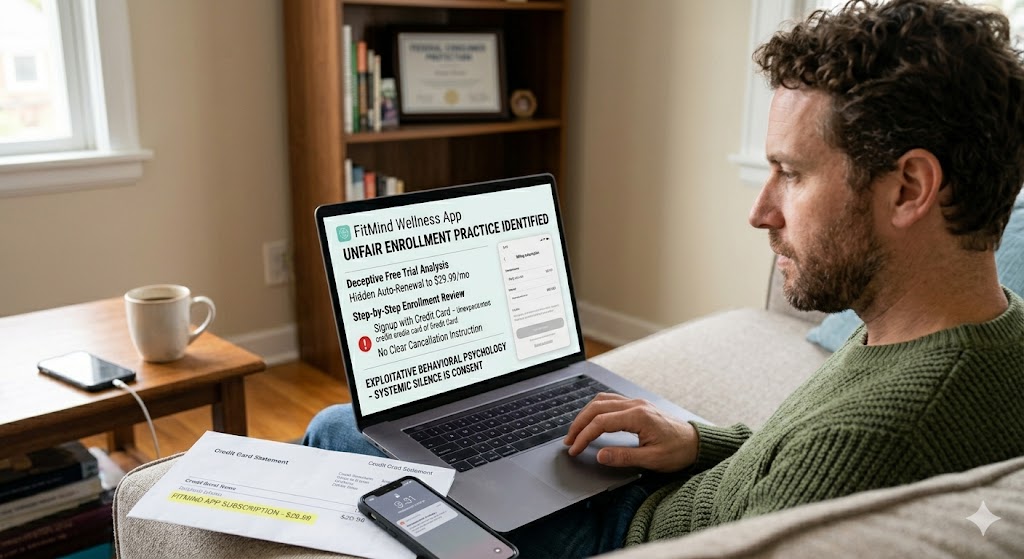

Automatic conversion to a paid subscription: once the trial ends, the app silently charges the stored payment method and often makes the cancellation path intentionally opaque.

The "free" label is therefore more of a marketing hook than a guarantee of zero cost. Because the transaction is initiated with a payment method, many consumer protection rules that apply to pure free offers (like clear “no charge” language) simply do not kick in. This specific setup makes it incredibly easy for companies to initiate hidden subscription fees under the guise of an open transaction, effectively neutralizing standard consumer financial protection mechanisms. When software platforms deploy these systems, they often exploit negative option marketing loops that treat user silence as systemic consent to be charged repeatedly.

Why Federal Oversight Falls Short Against Deceptive Billing Practices

At the federal level, AI-powered wellness apps sit in a regulatory gray zone. The FDA classifies low-risk devices (Class I) as exempt from review, meaning they can be marketed without any pre-market clearance. Most diet tracking or metabolic prediction tools fall into this category because they are deemed low risk. According to official guidelines from the Food and Drug Administration, general wellness applications that simply encourage weight loss or track food intake are intentionally exempted from strict medical review cycles.

Class II devices, which are moderate risk, usually require a 510(k) pre-market notification, but the majority of AI wellness apps do not meet the criteria that would push them into this higher risk bucket. Adding to the ambiguity, there is little oversight for AI-driven wellness apps overall. A recent Harvard Gazette analysis notes that the federal landscape offers “not much” supervision for these tools. Even an executive order on AI never substantially altered the FDA’s approach to such software.

Finally, the traditional distinction between general wellness devices and medical devices does not capture AI-enabled wellness apps, allowing most to slip through existing regulatory gaps. Because these tech platforms operate outside strict medical regulations, they face minimal systemic friction when executing deceptive billing practices. Traditional consumer financial protection acts are built around banking frameworks rather than dynamic app stores, creating a perfect structural environment for sophisticated free trial scams to flourish online.

Red Flags in the Fine Print: Spotting Automatic Renewal Clauses

If you are scanning the terms before you click “Start Free Trial,” keep an eye out for these warning signs:

Vague subscription language: phrases like “your plan will continue unless you cancel” without a clear deadline.

Auto-renewal clauses buried in footnotes: look for the words “auto-renewal,” “recurring billing,” or “continuous service” hidden in the middle of a paragraph.

No explicit cancellation instructions: a missing or hard-to-find “Cancel Subscription” link is a classic trap.

Health claim disclaimer: statements that the app is “not a medical device” without any FDA classification disclosure.

One-sided refund policy: language that limits refunds to “technical issues only” or requires a lengthy dispute process.

These red flags often signal that the free trial is a gateway to a recurring charge. Unscrupulous application developers use automatic renewal clauses to keep consumers locked into multi-month cycles without explicit, ongoing confirmation. Finding these automatic renewal clauses requires looking past the colorful checkout buttons and scanning the deep layers of the legal text where the core elements of negative option marketing are typically legally authorized by the consumer.

What the FTC Is Looking At Regarding Negative Option Marketing

The Federal Trade Commission has begun to scrutinize the practice of offering “free” wellness trials that automatically convert to paid subscriptions. While the agency’s investigations are ongoing, the precise legal outcomes remain uncertain. What is clear is that the FTC views deceptive auto-renewal practices as potentially unfair or deceptive under its consumer protection mandate. According to legal updates tracking federal enforcement actions, the regulatory body continues to struggle with enforcement because digital dark patterns evolve much faster than administrative legislation can adapt.

A primary area of concern for federal investigators is how negative option marketing systems exploit behavioral psychology to secure ongoing payments. When a consumer signs up for a trial, they focus heavily on the immediate health benefits, such as tracking body mass index or monitoring macronutrients. The app architecture deliberately downplays the transition from a free user to a paid subscriber. Because federal frameworks require lengthy periods to establish new rules, individual consumer financial protection remains the primary defense for internet users navigating these complex digital health platforms.

How to Verify Before You Commit to Avoid Free Trial Scams

A disciplined verification routine can protect you from surprise charges:

Read the subscription terms line by line: focus on sections titled “Billing,” “Renewal,” and “Cancellation.”

Search for a clear cancellation path: a dedicated “Cancel” button in the app’s settings or a short link in the email confirmation.

Check for FDA classification: reputable apps will disclose whether they are a Class I exempt device or have pursued a 510(k) clearance.

Look up consumer complaints: browse forums, the Better Business Bureau, or the FTC’s complaint database for patterns of auto charge disputes.

Confirm the trial length and post-trial price: the fine print should state the exact number of free days and the subsequent monthly or annual fee.

Test the support channel: send a quick inquiry about canceling; a prompt, helpful response is a good sign.

You can let EyeQ scan the app’s terms and surface hidden automatic renewal clauses in seconds, giving you a clearer picture before you enter payment details. Utilizing automated scanning systems ensures that sophisticated deceptive billing practices are flagged immediately, keeping your payment methods completely safe from predatory online free trial scams.

- Credit‑card required: Even “free” trials often ask for a payment method before you can start.

- Auto‑renewal hidden: Renewal terms are frequently buried deep in the terms‑of‑service.

- Refunds can be delayed: Many apps impose strict refund windows or require lengthy disputes.

- State enforcement varies: State consumer‑protection actions differ widely, and some jurisdictions have limited resources.

How ShouldEye Helps You Protect Your Consumer Financial Protection

ShouldEye aggregates three core data streams that make verification painless:

Trust signals: AI-driven analysis of a company’s registration, ownership, and any FDA disclosures.

Complaint analysis: Real-time aggregation of consumer complaints, chargeback disputes, and FTC filings.

Policy & fine print review: Natural language parsing of terms of service to highlight auto-renewal, cancellation friction, and hidden fees.

By feeding these signals into a single dashboard, ShouldEye lets you compare multiple wellness apps side by side, spot red flags, and decide whether the free trial is genuinely risk-free. The platform reinforces your baseline consumer financial protection by making dark patterns visible before any transactional authorization occurs.

Alternatives to the “Free Trial” Model

If the verification steps feel cumbersome, consider these lower-risk routes:

Evidence-based nutrition platforms that charge only after you have completed a baseline assessment.

Open source diet tracking tools that store data locally on your device, eliminating the need for a subscription.

Professional guidance: A registered dietitian can provide a personalized plan without the hidden auto-renewal mechanisms of many apps.

These options often come with clearer pricing structures and stronger consumer protections. Selecting open platforms or consulting accredited human experts completely eliminates the exposure to internet-based free trial scams and digital negative option marketing networks.

Final Thoughts

The allure of a free AI-powered diet plan can be strong, but the underlying enrollment mechanics frequently bypass the buyer protection safeguards that keep consumers safe. By understanding the regulatory blind spots, recognizing red flag language, and leveraging verification tools like ShouldEye and EyeQ, you can make an informed choice that aligns with your health goals and your wallet.

Before you click Start Free Trial, ask EyeQ to break down the hidden fees, cancellation steps, and any regulatory disclosures in seconds. A little due diligence today can save you from unexpected charges tomorrow. By addressing hidden subscription fees, evaluating automatic renewal clauses, and maintaining a high level of personal consumer financial protection, you can explore the latest wellness innovations without falling victim to internet deceptive billing practices. For more information on how regulatory bodies define online transparency, check out the consumer guidelines published by the Federal Trade Commission to understand your rights regarding digital billing. Additionally, you can review the official databases hosted by the Food and Drug Administration to verify if a health application is properly categorized under safe wellness parameters.

FAQs

What should I look for in the fine print of a free‑trial diet app?

Can the FTC stop an app from auto‑charging after a free trial?

Are AI‑driven diet apps regulated by the FDA?

How can I verify whether an app will charge me after the trial?

What are my options if I’m already auto‑charged?

Do I need a credit card to start a free trial?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.