A man and a woman use a tablet to analyze a large whiteboard presentation that contrasts baseline interest rates with fully loaded APR borrowing costs.

PhotogeminiAPR vs. Interest Rate: What’s the Real Difference?

Learn how APR and interest rate differ, why each matters, and how to verify loan costs before you sign. Get clear guidance on true borrowing costs.

When you shop for a loan, whether it’s a mortgage, auto loan, or personal line of credit, you’ll see two percentages on the offer sheet: the interest rate and the annual percentage rate (APR). At first glance, they look interchangeable, but each tells a different story about what you’ll actually pay. This guide walks you through the mechanics, highlights the pitfalls, and shows you how to verify the numbers before you sign. Financial intelligence tools like ShouldEye and EyeQ can assist you in parsing these figures to ensure transparency. Understanding the distinction between the baseline rate and the fully loaded cost protects your household budget from unexpected upfront spikes.

Evaluating the true financial impact of any debt instrument requires an accurate grasp of your true mortgage borrowing costs. Selecting appropriate financial paths involves investigating how extra charges alter your long-term obligations. To accurately calculate real loan costs, consumers must systematically assess every line item rather than accepting the base rate at face value.

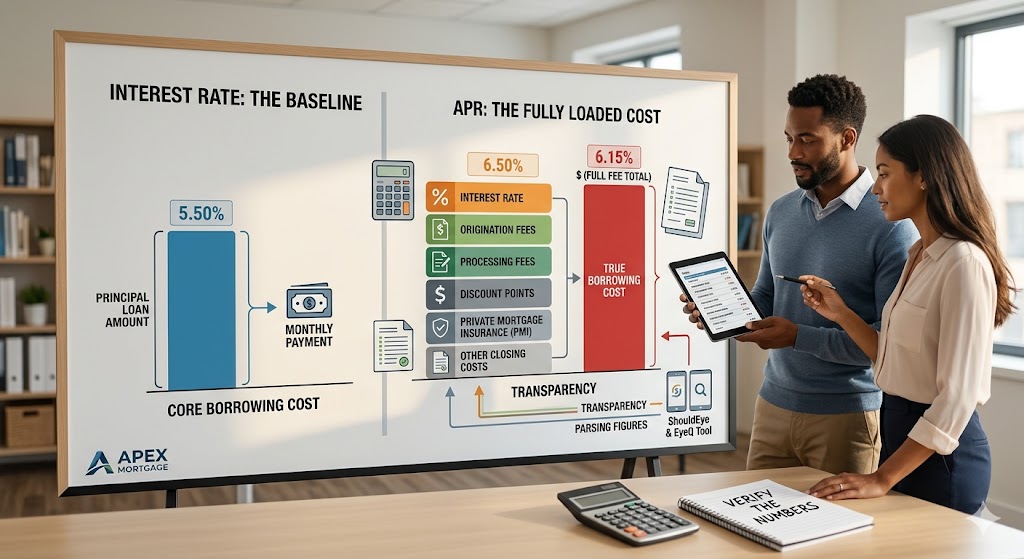

Interest Rate: The Basic Cost of Borrowing

The interest rate is the percentage a lender charges for borrowing money. It reflects the cost of using the principal balance and is the figure used to calculate your monthly payment. In other words, the lender applies the interest rate to the outstanding balance each month to determine how much interest you owe. For comprehensive federal guidelines on how rates operate under consumer protection laws, borrowers can consult the Federal Trade Commission for detailed guidance.

The interest rate is the percentage of your loan amount that the lender charges you as the cost of borrowing. Because the interest rate only covers the cost of borrowing the principal, it does not include any ancillary fees such as origination charges, processing fees, or insurance premiums. This is the raw cost of capital before administrative overhead is factored into the transaction.

APR: Adding Annual Percentage Rate Fees to the Picture

APR stands for Annual Percentage Rate. It starts with the same interest rate but adds any loan-related fees and costs to produce a single, annualized figure. The result is an effective rate that reflects the total cost of the loan over its term. Incorporating annual percentage rate fees into your analysis alters your perspective on which loan product is genuinely affordable.

APR includes the interest rate plus loan fees, offering a more complete picture of a loan’s overall cost. Because APR bundles fees into a single percentage, it lets you compare offers that have different fee structures. Two loans might have the same interest rate, but the one with higher fees will show a higher APR, signaling a higher overall cost. It serves as a regulatory leveling mechanism designed to prevent predatory lending structures.

Why the Two Numbers Matter to Your Wallet

The relationship between these percentages directly shapes your long-term liability. The interest rate shows the specific cost of borrowing the principal each month, which directly determines your monthly payment amount. Conversely, the APR reflects the total cost of the loan after fees are added, which helps you compare the true expense across lenders. To research industry-wide enforcement and common fair lending disclosures, borrowers can consult resources provided by the Consumer Financial Protection Bureau.

Even though monthly payments are calculated using the interest rate, not the APR, the APR tells you how much you’ll actually spend over the life of the loan. Ignoring fees can make a seemingly low-interest loan far more expensive. APR gives you a better idea of the real cost of the loan. Because the APR includes fees, you’ll have a better idea of how much you’ll actually pay when you compare APRs.

Common Misunderstandings and Home Loan Hidden Fees

A lower interest rate always means a cheaper loan is a common myth. Not necessarily; a low rate paired with high fees can result in a higher APR.

My monthly payment will be lower if the APR is lower, which is another misconception. Monthly payments are based on the interest rate; APR affects the total interest paid over time, not the payment amount.

All fees are included in the APR is false. Some lenders may exclude certain costs, such as pre-payment penalties, from the APR calculation. Always ask for a fee breakdown.

APR is the same for every state, which is inaccurate. Calculation methods can vary by jurisdiction, and regional administrative structures often influence final tallies.

Uncovering home loan hidden fees requires close inspection of early disclosure documents. Borrowers often overlook processing expenses that balloon the true cost of their capital over twenty or thirty years.

How to Verify the Numbers and Calculate Real Loan Cost Before You Sign

1. Request a Full Fee Schedule

Ask the lender for a line-item list of every charge that will be rolled into the APR. Typical fees include origination or processing fees, discount points, title and recording fees, and insurance premiums required by the lender.

2. Re-calculate the APR Yourself

Once you have the fee list, you can use an online APR calculator or EyeQ to input the interest rate, loan amount, term, and fees. This lets you see whether the lender’s disclosed APR matches the math. Use EyeQ to break down the APR calculation and see exactly which fees are rolled into the figure.

3. Compare Monthly Payments Separately

Since payments are based on the interest rate, verify that the payment schedule matches the advertised rate. A mismatch could indicate hidden costs or a misquoted rate.

4. Look for Hidden or Optional Fees

Even if a fee is optional, such as credit-life insurance, it may be included in the APR. Decide whether you need the optional add-on before it inflates the APR.

5. Check Regulatory Disclosures

In many jurisdictions, lenders must disclose the APR alongside the interest rate in a clear, standardized format. Verify that the disclosure meets local consumer-protection rules.

6. Use a Trusted Verification Tool

Before finalizing any loan, run the numbers through ShouldEye or a similar trust-intelligence platform to spot inconsistencies, hidden fees, or complaints about the lender’s APR practices.

How ShouldEye Helps You Check Home Loan Hidden Fees

ShouldEye aggregates public complaints, regulatory filings, and fee disclosures to give you a single dashboard of trust signals for any loan offer. By feeding the lender’s name and the advertised interest rate or APR into ShouldEye, you can easily verify mortgage borrowing costs.

Spot recurring fee-related complaints that may indicate undisclosed costs.

Compare the disclosed APR against industry averages for similar loan types.

Review the fine print for hidden clauses such as pre-payment penalties or mandatory insurance.

Run an AI-assisted risk check that flags any red-flag language or missing disclosures.

The platform’s complaint analysis and policy review features let you move beyond the headline numbers and understand the true cost of borrowing. To understand personal debt sustainability and structural borrowing terms, reviewing materials from the National Foundation for Credit Counseling offers deep foundational support. This ensures you can compare loan offers online with absolute confidence.

Next Steps to Compare Loan Offers Online with EyeQ

When you’ve gathered the interest rate, fee schedule, and APR, ask EyeQ to compare multiple offers side-by-side. It will highlight which loan has the lowest effective cost, point out any outlier fees, and even suggest questions to ask the lender before you sign. Before you lock in a loan, ask EyeQ to compare the APR and interest rate across offers in seconds.

By treating the interest rate and APR as complementary tools, rather than interchangeable, you’ll make a more informed borrowing decision and avoid surprise costs down the road. Understanding the distinction between annual percentage rate fees and simple interest is the first step toward transparent borrowing. Use the verification steps above, and let ShouldEye and EyeQ do the heavy lifting so you can focus on the loan that truly fits your financial goals. Use these tools to systematically calculate real loan cost parameters before signing any contract.

FAQs

What is the main difference between APR and interest rate?

Which number should I use to compare loan offers?

Are monthly payments calculated using APR or interest rate?

Can a loan have a low interest rate but a high APR?

Does APR affect my credit score?

How can I verify that a lender’s APR is accurate?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.