A group of financial analysts reviewing holographic ShouldEye EyeQ displays that show a "Recommended Consolidation Loan," a "Risk Analysis Map" with red flags, and a "Debt Repayment Strategy" checklist against a 2026 city skyline

PhotogeminiIs Debt Consolidation With a Personal Loan Actually Worth It?

Explore if a personal‑loan debt consolidation saves money, lowers payments, and fits your credit profile. Learn verification steps, risks, and how ShouldEye can help.

When credit card balances, payday loans, and other high-interest obligations pile up, the idea of rolling everything into a single personal loan can feel like a financial lifeline. A personal loan debt consolidation strategy promises a fixed rate, one monthly payment, and potentially lower overall interest. But the promise isn’t a guarantee. In this guide, we break down the mechanics, the hidden costs, and the questions you should answer before signing on the dotted line. To ensure you aren't falling into a predatory trap, tools like ShouldEye can help you verify the legitimacy of a lender’s claims, while EyeQ allows you to simulate the long-term impact on your net worth. Understanding these nuances is essential for any modern debt repayment strategy.

What Does a Personal Loan Debt Consolidation Look Like?

A debt-consolidation personal loan is simply a lump-sum loan that you use to pay off existing debts. The loan typically carries a fixed interest rate, which means your monthly payment stays the same for the life of the loan. Because the rate is fixed, you avoid the variable APRs that credit cards can charge, especially when market rates rise. In 2026, finding competitive consolidation loan interest rates is the primary driver for consumers looking to exit high-interest revolving cycles.

The process usually follows these steps:

Apply for a personal loan and receive a credit decision.

The loan amount is often directly deposited into your bank account.

Pay off each of your existing balances with the lump sum.

Make one monthly payment to the personal-loan lender.

If the loan’s APR is lower than the average APR of the debts you’re replacing, you could see interest savings. For example, a personal loan at 10% APR over 24 months generates about $790 in total interest, compared with $13,332 in interest on three credit cards at 24% APR over 319 months. This stark difference is why many look toward an installment loan credit score impact as a secondary benefit to the immediate cash flow relief. For more data on national average rates, the Federal Reserve provides updated consumer credit reports.

Potential Benefits

Using a personal loan for credit card debt relief offers several predictable advantages. A fixed monthly payment allows for predictable budgeting with no surprise rate hikes. Simplified finances mean you have one due date instead of juggling multiple cards. Furthermore, the potential interest savings can be massive if you secure a lower APR than what high-interest credit cards charge. There is also a credit score boost potential; paying off revolving balances can improve your utilization ratio, which is a key factor in your credit profile.

EyeQ tip: Use EyeQ to run a quick interest-savings calculator that compares your current credit-card APRs with a sample personal-loan rate.

Key Factors to Evaluate Before You Commit

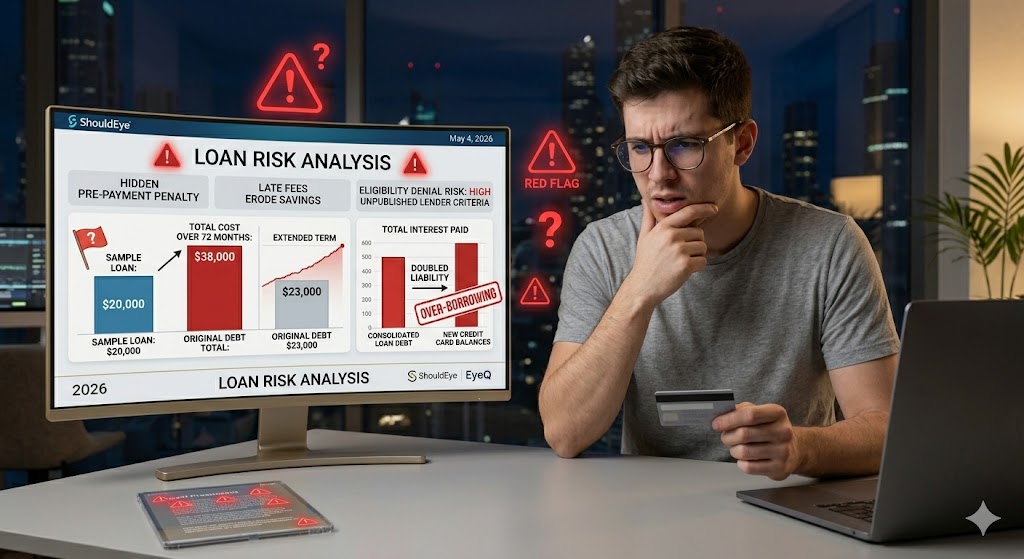

Before diving into a personal loan debt consolidation, you must evaluate several critical factors. First is the interest rate versus existing debt. The loan must be offered at a lower rate than the weighted average of your current debts. If the gap is small, any savings may be eaten by personal loan origination fees, which often range from 1% to 5% of the total loan amount.

Next, consider the loan term length. Extending the term lowers the monthly payment but can significantly increase the total interest paid over time. You must also satisfy credit score requirements; borrowers with poor credit may only qualify for rates that are comparable to their current cards, nullifying the benefit. Additionally, be aware of collateral risks. While many personal loans are unsecured, some are secured by assets like a home or car. Missing a payment on a secured loan can jeopardize that asset. Finally, the installment loan credit score impact is real; opening a new account causes a short-term dip due to a hard inquiry, though the long-term utilization improvement often offsets this. For a detailed breakdown of how inquiries affect you, visit MyFICO.

Common Pitfalls and Red Flags

Many borrowers fall into traps involving hidden fees, such as pre-payment penalties or late-payment fees that erode savings. Eligibility uncertainty is another issue, as lenders rarely publish their exact criteria, leading to unexpected denials or high-rate offers. One of the biggest mistakes is assuming a lower monthly payment always equals a better deal; a longer term might feel easier on the wallet today, but cost thousands more in the long run. There is also the risk of over-borrowing, where consumers consolidate their debt but then immediately run up their credit card balances again, doubling their total liability.

How to Decide If It’s Worth It for You

To determine if this debt repayment strategy is right for you, start by gathering your current debt data: list each balance, APR, and minimum payment. Calculate the weighted-average APR of your existing debt and obtain a personal-loan quote, including all personal loan origination fees, from at least two lenders.

Run the numbers to compare the total interest on existing debt versus the total interest on the loan. Look at the monthly payment comparison and the total cost over the life of each option. Also, consider non-financial factors like your comfort with a single payment and how the loan fits your long-term credit-building goals. Stress-test the scenario: what happens if you miss a payment? Does the loan have a grace period?

If the consolidated loan shows a clear, net-positive interest saving and a manageable monthly payment, it may be worth pursuing. If fees or a higher term erase the advantage, look at alternative credit card debt relief strategies such as balance-transfer cards or debt-management programs.

How ShouldEye Helps You Check This

ShouldEye aggregates publicly available complaint data, fee disclosures, and lender-policy language into a single view. By entering the lender’s name into ShouldEye, you can spot recurring complaints about hidden fees or aggressive collection practices. It allows you to verify fee structures to see whether personal loan origination fees are typical for that specific lender. You can also compare policy language to understand pre-payment penalties or collateral requirements. By running a side-by-side comparison of multiple lenders’ trust signals, ShouldEye helps you prioritize offers with the cleanest track record. The platform’s AI-driven analysis saves you hours of manual research and highlights red flags you might otherwise miss in the fine print of consolidation loan interest rates.

- Rate Gap Matters: A lower APR than your current debts is the primary driver of savings.

- Fees Can Erase Gains: Origination or closing fees may consume the interest advantage.

- Credit Profile Is Key: Borrowers with poor credit often receive rates that match or exceed credit‑card APRs.

- Missed Payments Carry High Risk: Especially on secured loans, a missed payment can jeopardize collateral.

Using EyeQ to Make a Smarter Choice

Before you finalize any loan, ask EyeQ to compare the total cost of your current credit card balances versus a specific personal loan offer. EyeQ can factor in a 10% interest rate with a 2% origination fee instantly, revealing whether the consolidation truly saves you money or just shuffles the debt around. This data-driven approach ensures your personal loan debt consolidation is a mathematical victory rather than an emotional guess.

Final Thoughts

Debt consolidation with a personal loan can simplify finances and, under the right conditions, lower the amount of interest you pay. The decision hinges on three pillars: rate advantage, fee transparency, and your credit profile. Treat the loan as a tool and not a cure, and always run the math before you sign. By combining the trust signals from ShouldEye with the analytical power of EyeQ, you can navigate the complex world of RWA crypto investing or traditional personal finance with equal confidence. Invest wisely and remember that the best debt repayment strategy is the one that actually gets you to a zero balance.

FAQs

Can a personal‑loan consolidation eliminate my debt?

Will consolidating always lower my monthly payment?

Do all personal loans have origination fees?

How does a consolidation loan affect my credit score?

Is a secured personal loan riskier than an unsecured one?

What should I look for in lender reviews before consolidating?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.