A professional woman stands at a literal crossroads between two neon highway signs labeled "Fixed-Rate Loan" and "Variable-Rate Loan," pondering her financial options amid floating digital icons of credit scores, budgets, and a balance scale.

PhotogeminiFixed-Rate vs Variable-Rate Personal Loans: Which Is Safer for Beginners?

Explore the pros, cons, and risk factors of fixed‑rate and variable‑rate personal loans. Learn how beginners can verify terms, spot red flags, and decide wisely.

When you take your first personal loan, the rate structure is one of the first decisions you will face. Fixed-rate loans lock in a single interest rate for the life of the loan, while variable-rate loans usually start lower but can shift as market conditions change. For beginners, the trade-off between predictability and potential savings can feel like a gamble. This guide walks you through the mechanics of each rate type, highlights the questions you should ask before you sign, and shows how to use trust intelligence tools to keep the process transparent. Using ShouldEye to cross-reference modern loan practices ensures you do not get caught in predatory lending cycles. Understanding how interest rates affect your monthly obligations is essential before signing any contract. Evaluating your personal financial budgeting strategy allows you to see how much room you have for fluctuating costs. Your credit scores will also play a massive role in determining which rate structure offers the lowest baseline cost. Managing long-term debt management goals requires balancing immediate savings with future safety. Navigating complex loan terms does not have to be overwhelming when you have automated compliance tools at your disposal.

Understanding Fixed-Rate Personal Loans

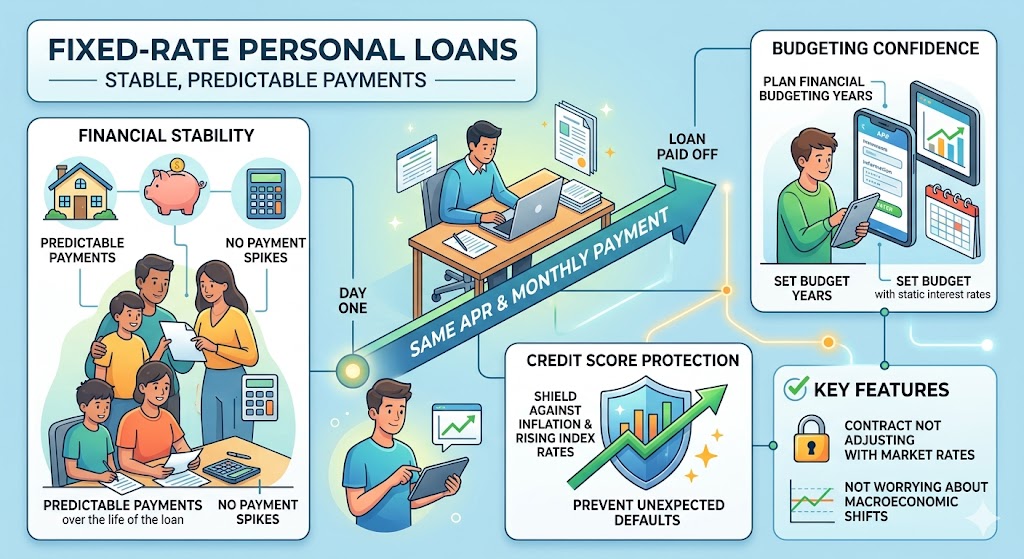

A fixed-rate personal loan guarantees the same APR and monthly payment from day one until the loan is paid off. The stability comes from a contract that does not adjust with the broader interest rate environment. Research from authoritative financial bodies highlights that fixed-rate personal loans offer stable, predictable payments over the life of the loan.

This predictability is especially comforting for borrowers who prefer a set budget and want to avoid surprise payment spikes. When analyzing personal loans, stability is often the top priority for those entering the credit market for the first time. Having static interest rates means you can plan your financial budgeting for years without worrying about macroeconomic shifts. While you might miss out on savings if market rates plummet, the protection against inflation and rising index rates is a significant shield for your credit scores. It prevents unexpected defaults, keeping your debt management plan perfectly on track throughout the entire loan term.

What to verify

APR disclosure: The loan’s APR should be listed in the offer and remain unchanged.

Fee schedule: Origination, pre-payment, and late payment fees must be spelled out clearly.

Repayment term: Ensure the term matches the payment schedule you have calculated.

Understanding Variable-Rate Personal Loans

Variable-rate loans typically begin with a lower, more competitive rate than their fixed counterparts. Financial briefs state that the advantage a variable-rate personal loan has over a fixed-rate loan is that you typically start with a lower, more competitive rate. However, the rate can rise or fall based on an index plus a margin set by the lender. If interest rates increase, your monthly payment can climb, sometimes dramatically. Variable loans also often allow you to pay interest only on the amount you draw, similar to a line of credit.

This flexibility can be useful if you need cash intermittently, but it adds another layer of complexity to personal loans. Beginners must carefully calculate whether their financial budgeting can absorb a worst-case scenario rate hike. A sudden jump can damage credit scores if payments become unaffordable, turning a short-term solution into a long-term debt management crisis. Always look at the maximum ceiling within the loan terms to ensure compliance with your personal risk tolerance.

What to verify

Rate index and margin: The contract should name the benchmark and the lender’s added percentage.

Rate caps: Look for a maximum rate or periodic increase limit that protects you from runaway hikes.

Adjustment frequency: Know whether the rate changes monthly, quarterly, or annually.

Key Considerations for Beginners

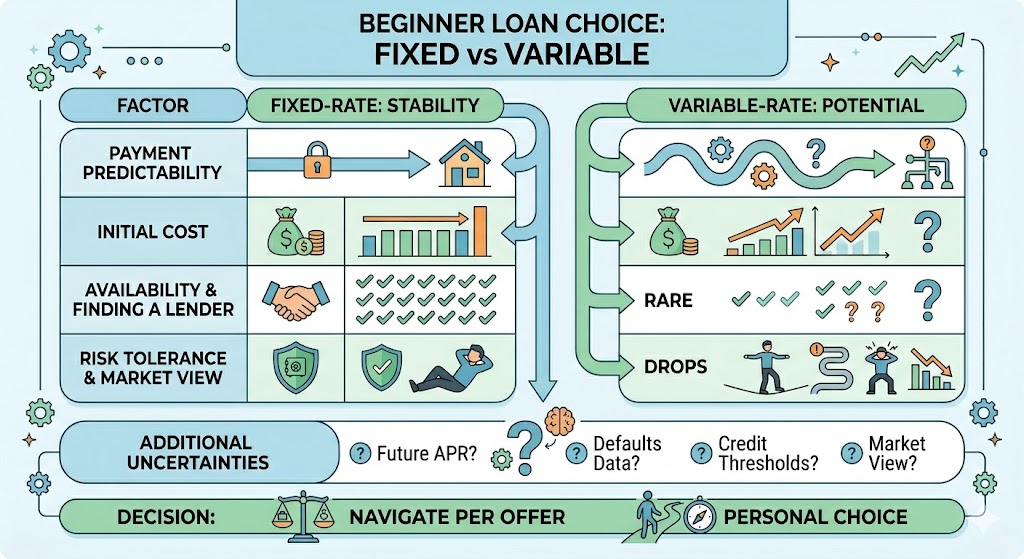

When evaluating payment predictability, fixed-rate personal loans keep payments exactly the same, aiding your monthly financial budgeting. On the other hand, variable-rate personal loans cause payments to change, requiring highly flexible cash flow. Looking at the initial cost, fixed options may start higher than variable offers, while variable rates usually offer lower start-up interest rates, though future increases remain possible.

In terms of availability, more lenders offer fixed-rate personal loans. Many borrowers have a harder time finding a lender willing to give them a variable-rate loan. For risk tolerance, fixed rates suit borrowers uncomfortable with financial risk, whereas variable rates suit those who can absorb rate swings or expect market trends to drop. Your credit scores will dictate the baseline offers you receive for both structures. If you want to maintain clean debt management habits, reading the exact loan terms is non-negotiable.

There are several uncertain factors you will need to research independently before committing to an offer. Exact APR ranges for both rate types are not publicly compiled on a global scale. Default or delinquency statistics for beginners using each rate type are rarely disclosed transparently by individual firms. Furthermore, credit score thresholds that separate fixed-rate from variable-rate offers remain opaque across major banking institutions. The broader market availability of variable-rate personal loans beyond a few select lenders is often unclear. Because these data points can vary wildly, the safest approach is to treat each loan as a case-by-case decision rather than relying on a blanket rule.

How to Verify Loan Terms Before You Commit

Read the fine print: Focus on the APR, interest rates, index, margin, and any caps.

Ask for a written rate-change schedule: Lenders should provide a clear timeline of when adjustments can occur.

Compare at least three offers: Use a neutral aggregator like the Consumer Financial Protection Bureau or NerdWallet to see how different lenders present the same information.

Check for hidden fees: Look for pre-payment penalties, processing fees, or early termination charges.

Run an EyeQ check: You can fire up EyeQ to pull the lender’s complaint history, policy summaries, and any red flag signals in seconds.

Confirm flexibility: If you think you might want to refinance later, verify whether the loan allows early payoff without penalty.

Consider how major institutions frame these options. Citi notes that variable-rate loans can be harder to find, hinting that many borrowers will encounter fixed-rate options first. OneMain Financial markets its fixed-rate personal loans by emphasizing clear terms and fast decisions. Popular financial aggregates list personal loans that are predominantly fixed-rate, emphasizing that the APR and payment won’t change over the loan’s life. These examples show how the same rate type can be framed differently across providers, impacting your financial budgeting and debt management timeline. Always ensure your credit scores are optimized before applying to lock in the best possible loan terms.

- Payment predictability: Fixed‑rate loans keep your monthly payment the same, while variable loans can change.

- Initial cost: Variable loans often start with a lower APR, but that advantage can disappear if rates rise.

- Market availability: Most lenders readily provide fixed‑rate personal loans; variable options are less common.

- Risk tolerance matters: Your comfort with uncertainty should guide the rate type you choose.

How ShouldEye Helps You Check This

ShouldEye aggregates three core trust signals for any personal loan offer to protect consumers from bad deals. Our systems conduct a thorough complaint analysis by scanning consumer forums, Better Business Bureau filings, and regulator reports to surface patterns of late payment fees, hidden charges, or poor customer service. We also perform a policy and fine print review where our automated systems extract interest rate caps, pre-payment penalties, and rate adjustment clauses, presenting them in plain language.

Finally, our alternative comparison engine lines up fixed and variable options from multiple lenders, highlighting where terms diverge. By feeding the loan documents into ShouldEye, you get a concise risk dashboard that tells you whether the lender’s disclosures are transparent, whether the rate change mechanics are reasonable, and how the offer stacks up against peers, keeping your financial budgeting safe and your credit scores protected. Proper debt management relies on understanding these exact loan terms.

Using EyeQ to Make a Smarter Choice

Before you click accept, ask EyeQ to break down the fine print, hidden fees, and any rate cap limits on your personal loans. EyeQ can also flag whether the lender has a history of changing terms after onboarding, giving you a clearer picture of the long-term cost. Evaluating interest rates over time is critical for stable financial budgeting. Protecting your credit scores requires vigilance against sudden payment spikes, making automated fine print analysis a vital part of modern debt management. Don't let complex loan terms catch you off guard when automated intelligence can verify compliance instantly.

Bottom Line for Beginners

Neither rate type is universally safer. A fixed-rate loan gives you budgeting confidence, which many beginners find essential for long-term financial budgeting. A variable-rate loan can be attractive if you expect interest rates to stay low, you have a flexible cash flow, and you are comfortable monitoring the shifting market. The decisive factor is how much uncertainty you are willing to tolerate within your personal loans. Protecting your credit scores and maintaining healthy debt management habits should always be your guiding light when reviewing loan terms.

Your next step is to gather at least three loan offers, run them through ShouldEye, and fire up EyeQ to surface any hidden risk. With those insights, you will be able to choose the rate structure that aligns with your financial comfort zone. Ready to verify a loan before you sign? Use EyeQ to compare trust signals, complaints, and policy risks in seconds.

FAQs

What is the main difference between fixed‑rate and variable‑rate personal loans?

Are fixed‑rate loans always safer for beginners?

What should I verify before signing a personal loan?

Can I switch from a variable‑rate loan to a fixed‑rate loan later?

How do I know if a variable‑rate loan will stay low?

Do all lenders offer both fixed and variable personal loans?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.