How Do Personal Loans Work? Monthly Payments, APR, and Fees Explained Simply

Learn how personal loans work, from interest rates and APR to monthly payments and origination fees. Get clear guidance to verify loan terms before you sign.

How Do Personal Loans Work? Monthly Payments, APR, and Fees Explained Simply

When you see a personal loan offer, the headline numbers—interest rate, monthly payments, APR - can feel like an impenetrable code you need to crack before you can access the funds you need. Whether you are looking to consolidate high-interest credit card debt, fund a major home improvement project, or cover an unexpected medical emergency, understanding the mechanics of personal loans is absolutely essential.

Unfortunately, the financial industry often relies on complex jargon that obscures the true cost of borrowing. Understanding what each term means, how these various elements interact with one another, and where hidden loan costs typically hide is the crucial first step toward finding a loan that fits comfortably into your budget instead of surprising you with unaffordable bills later.

This comprehensive ShouldEye guide walks through the core components of personal loans, highlights the financial trade‑offs of different loan terms, explains the impact of your credit history, and shows you exactly what you need to verify in the fine print before you sign on the dotted line.

The Foundation: How Your Credit Score Influences Your Loan

Before diving into the specific mechanics of a loan agreement, it is important to understand how lenders determine the numbers they offer you in the first place. When you apply for personal loans, lenders evaluate your credit score, credit history, and debt-to-income ratio to assess how risky it is to lend you money.

Borrowers with excellent credit scores (typically 720 and above) are usually offered the most favorable terms. This means they receive the lowest interest rates, higher borrowing limits, and are often able to secure loans that do not charge origination fees. On the other hand, borrowers with fair or poor credit will likely see much higher rates and steeper fees to offset the lender's perceived risk. Knowing where your credit stands before you apply gives you a realistic expectation of the rates you will qualify for and helps you spot an offer that might be predatory.

What’s Inside a Personal Loan Agreement?

A personal loan agreement is a legally binding contract between you and the lender that spells out every detail of your borrowing arrangement. This includes the base interest rate, the full repayment term, the exact amount you are borrowing, and any fees or penalties you may face during the life of the loan.

Some lenders also provide a separate truth-in-lending disclosure or a summary letter that lists the monthly payments, the APR, and the full repayment schedule. You should treat both of these documents as the foundational legal blueprint of your borrowing relationship. Any deviation from what is written in these documents can become a serious dispute point later. You should look closely at clauses regarding default definitions (what exactly constitutes a missed payment) and whether there is any grace period before late fees are applied.

Understanding Interest Rate vs. APR

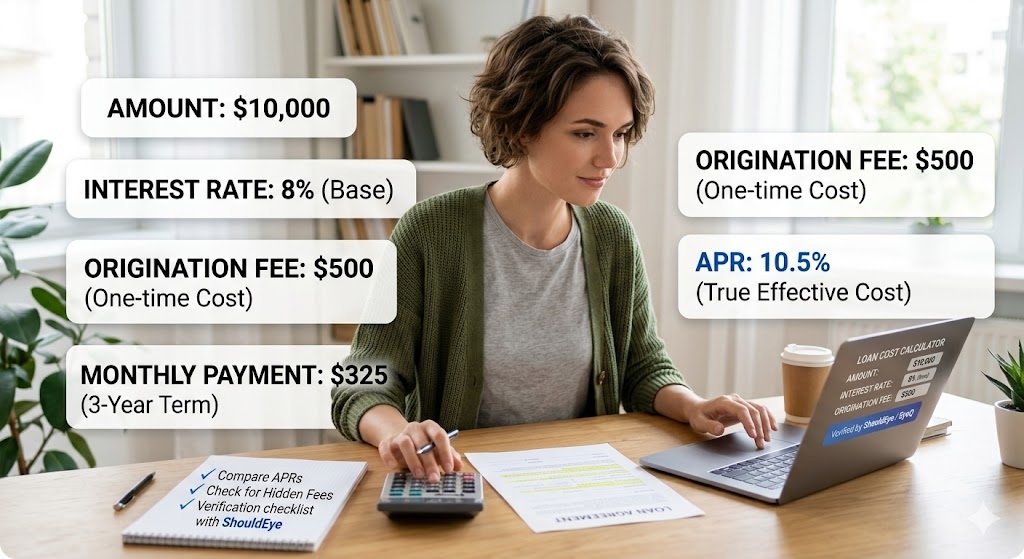

One of the most common areas of confusion for borrowers is the difference between the base interest rate and the Annual Percentage Rate. Understanding the APR vs interest rate distinction is vital for accurate comparison shopping.

The interest rate is strictly the base charge a lender applies to the principal amount you borrow. It does not account for any additional expenses.

The APR, on the other hand, reflects the total effective cost of the loan after all mandatory loan‑related expenses - such as origination fees and administrative charges - are added into the calculation and annualized.

For example, imagine you are borrowing $10,000 at an 8% interest rate, but the lender charges a 5% origination fee ($500). If you look only at the interest rate, you might think the loan is cheaper than a competing offer of 9% with no fees. However, when that $500 fee is factored into the APR over a three-year term, the true annualized cost of the first loan is actually much higher. In plain language, the APR tells you how much the loan truly costs each year, making it the most reliable and accurate figure for comparing multiple offers.

How Monthly Payments Are Calculated

While the exact mathematical formula (known as the amortization equation) is highly technical, you do not need to memorize it to understand how your bill is structured. Most lenders and consumer‑finance websites offer user-friendly online calculators where you simply input three numbers: the loan amount, the APR, and the repayment period.

The tool then returns the estimated monthly payments and the total cost over the life of the loan. It is important to know that in the early months of your loan, a larger portion of your payment goes toward paying off the interest, while a smaller portion reduces the principal balance. As time goes on, this ratio flips. Running a quick check with a loan calculator helps you see whether a proposed payment fits comfortably into your monthly cash flow without straining your budget.

The Role of Origination Fees and Hidden Costs

Many lenders charge origination fees to cover the administrative costs of underwriting and processing the loan. This is a one‑time upfront cost, and lenders handle this fee in two common ways:

They deduct it directly from the loan amount before the funds are disbursed. For instance, if you borrow $10,000 with a $500 fee, you only receive $9,500 in your bank account, but you are still responsible for paying back the full $10,000 plus interest.

They roll the fee into your principal balance, meaning you borrow $10,500 total, which increases your monthly payments and the total interest you will pay over time.

Origination fees are not the only expenses to watch out for. Other hidden loan costs can include steep late payment fees, non-sufficient funds fees if your automatic bank draft bounces, and payment processing fees if you choose to pay by phone or with a debit card instead of a direct bank transfer.

Short vs. Long Loan Terms and Prepayment Penalties

The length of your loan dictates a massive portion of your overall financial commitment. Understanding the trade‑offs between different loan terms allows you to choose an arrangement that balances short-term affordability with long-term cost efficiency:

Shorter terms (e.g., 12‑36 months): These usually carry much lower interest rates but result in significantly higher monthly payments. The lower rate can help offset the impact of an origination fee, but you will need enough disposable income in your budget to comfortably meet the larger payment every month.

Longer terms (e.g., 60‑84 months): Stretching the loan over five to seven years dramatically lowers the monthly payment amount, making the loan feel much easier on a tight budget. However, lenders typically apply higher interest rates to longer‑term loans to account for the extended risk. Furthermore, paying interest over 84 months drastically raises the total amount of money you repay over time.

Additionally, always check the contract for a prepayment penalty. Some lenders penalize you for paying off your loan early because it deprives them of the interest they expected to collect. You always want a loan that allows you to make extra principal payments or pay off the entire balance early without any extra charges.

Common Red Flags to Verify Before You Sign

Before you click accept or sign any paperwork, run a thorough verification checklist to ensure you are getting a fair, legitimate deal and avoiding predatory lending traps:

Missing or vague fee disclosures: The loan agreement should clearly and explicitly list any origination fees, late‑payment penalties, or pre‑payment penalties in standard dollar amounts or exact percentages.

Inconsistent APR vs. interest rate: The APR should always be equal to or higher than the base interest rate. If there is a massive, unexplained mismatch between the two numbers, the lender may be hiding undisclosed costs.

Unclear repayment schedule: Ensure the exact monthly payment amount, the specific due date each month, and the accepted payment methods are spelled out in writing.

Guaranteed approval claims: Legitimate lenders always check your credit and financial history. If a lender promises guaranteed approval without looking at your credit, it is likely a scam or a predatory payday loan in disguise.

No contact information for the lender: A legitimate, trustworthy lender will always provide a verified physical address and a reachable, responsive customer‑service line.

If any of these items are absent, confusing, or buried in illegible fine print, you should immediately pause the process and request written clarification.

How ShouldEye Helps You Check This

ShouldEye’s AI‑driven platform is designed to completely automate the tedious verification steps outlined above. By uploading a loan agreement or entering the key terms into the system, you can easily protect yourself:

Extract trust signals: The system instantly verifies licensing information, business registration numbers, and aggregated third‑party reviews to ensure the lender is legitimate.

Analyze complaint patterns: ShouldEye scans across public consumer‑complaint databases to spot recurring issues, such as lenders who illegally hold funds or apply phantom fees.

Parse fine print: The AI reads through the dense legal jargon to flag hidden loan costs, predatory penalty clauses, binding arbitration requirements, and ambiguous language that could trap you later.

Compare alternatives: By using the same standardized criteria, you can clearly see how one loan stacks up against competing offers without needing to do any manual spreadsheet work yourself.

Run a risk assessment: The platform flags regulatory red flags or unusually high gaps between the APR and the base rate, warning you of potentially predatory terms before you sign.

🧠 ShouldEye Insight A personal loan’s true cost lives deep in the APR calculation and the underlying fee structure, not just in the flashy headline interest rate you see in an advertisement. ShouldEye surfaces those buried costs and meticulously cross‑checks the lender's reputation, giving you a completely clear, unbiased picture of the financial commitment before you commit your signature.

Next Steps with EyeQ

By combining a solid understanding of fundamental loan mechanics with powerful, automated verification tools, you can move forward with total confidence—or know exactly when to walk away from a bad deal when the numbers simply do not add up.

When you are ready to proceed, use EyeQ to run a comprehensive trust check on the lender’s terms before you sign. It will automatically surface any missing disclosures and immediately flag unusual or predatory fee patterns. You can ask EyeQ to instantly break down the fine print, enumerate all potential fees, and map out your true repayment schedule in seconds, empowering you to compare multiple offers side-by-side without spending hours digging through dense, confusing PDF documents.

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.