A woman in a cafe carefully checks her smartphone while digital verification overlays from ShouldEye and EyeQ flag P2P payment safety metrics next to a mobile banking app screen.

PhotogeminiPeer-to-Peer Payment Fraud: Protecting Your Zelle and Venmo Transfers

Learn proven steps to verify contacts, enable security, and react to scams on Zelle and Venmo. Get a practical checklist and see how ShouldEye can help.

Peer-to-peer (P2P) payment apps make it effortless to move money, but that convenience also creates a fertile ground for fraud. Whether you’re sending cash to a roommate, paying a freelancer, or splitting a dinner bill, a single mistake can turn a routine transfer into a loss that’s hard to recover. To keep your money secure, digital wallet security must become a central part of your routine. Utilizing intelligence tools like ShouldEye and EyeQ can bridge the safety gap by flagging deceptive accounts before you hit send. This comprehensive guide explains the most common mobile payment scams targeting platforms like Zelle and Venmo, outlines what these services actually cover, and provides a verification strategy to ensure every transaction remains secure.

Understanding peer-to-peer transfer safety requires a shift in how we view financial applications. When you use these networks, you are essentially operating within an environment where speed overrides traditional banking safety nets. For a deep dive into the official security architectures of digital finance, the Federal Trade Commission provides extensive resources on how electronic fund ecosystems operate and how digital wallet security can be compromised by social engineering.

Understanding the Risk Landscape and Mobile Payment Scams

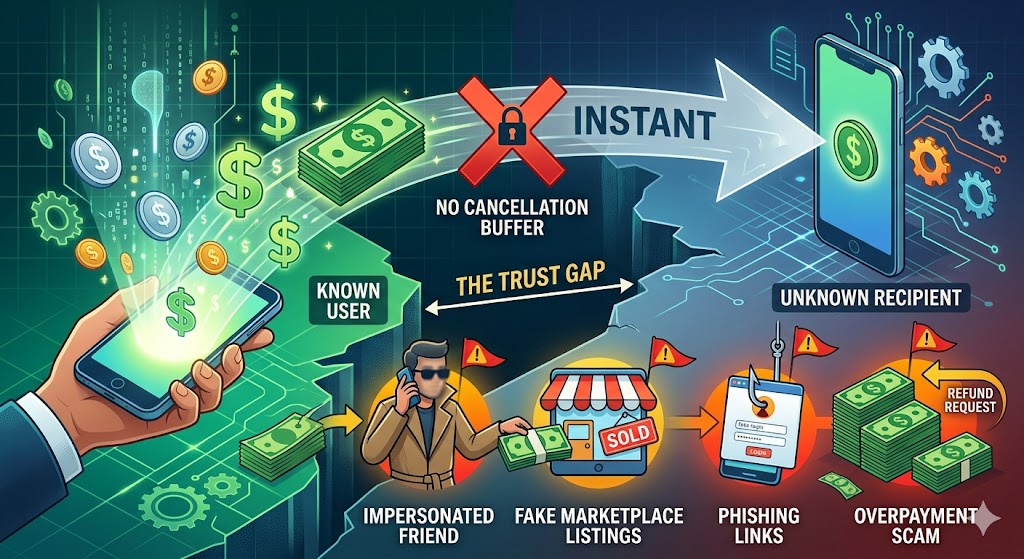

Zelle, Venmo, and similar applications treat each financial transaction as if you were handing physical cash directly to the recipient. The cash-like nature of these ecosystems means there is usually no built-in fraud protection or structural mechanism to cancel a transfer once it has been accepted by the receiving party. While these platforms embed rigorous security layers such as advanced data encryption, multifactor authentication, and back-end fraud controls, those safeguards protect the user account from unauthorized login access rather than protecting the individual transaction itself from p2p fraud prevention failures.

Because money moves instantly across these networks and appears in the recipient’s available balance within seconds, digital criminals actively exploit the trust gap that exists between a known contact and an unknown sender. The result is a rising tide of consumer reports detailing severe financial losses due to mobile payment scams, especially when users deviate from established p2p fraud prevention habits. This lack of a transaction buffer means that once the data is processed, the sender bears the full brunt of the financial liability.

Common Mobile Payment Scams and Scam Tactics

The methods deployed by financial fraudsters evolve constantly, but they generally rely on psychological manipulation to bypass your standard digital wallet security checks. By understanding these specific peer-to-peer transfer safety vectors, you can identify anomalies before any capital leaves your checking account.

Impersonated Friend

A fraudster pretends to be a friend, family member, or coworker in urgent need of immediate cash. They often compromise a legitimate account or create a lookalike profile using stolen profile pictures to bypass your digital wallet security. The major red flag here is an unexpected request paired with an emotionally distressing story that pressures you to act immediately without verifying the recipient's true identity.

Fake Marketplace Listings

A buyer or seller posts a highly appealing, too-good-to-be-true offer on a public classifieds site or social network and insists on receiving payment through Zelle or Venmo. They often refuse traditional e-commerce payment methods that offer buyer protections. The critical warning sign is when a vendor demands that a transaction be completed entirely outside the official marketplace checkout flow, specifically targeting channels that lack Zelle protection rules or Venmo fraud liability coverages.

Phishing Links

Users receive an email or text message containing a hyperlink that looks identical to the official mobile payment login screen. The text usually claims your account has been locked due to suspicious activity. The clear indicators include misspelled URLs, urgent text warnings, and direct requests to input your password, PIN, or multi-factor authorization codes into an unverified digital interface.

Overpayment Scam

A scammer sends a fraudulent or stolen check to your account or uses an unauthorized credit card to push an inflated balance to your wallet. They then contact you, claiming they sent too much money by mistake, and ask you to refund the difference via an immediate peer to peer transfer safety method. The initial payment eventually bounces or gets reversed by the bank as p2p fraud prevention systems identify the stolen funding source, leaving you completely out of pocket for the refunded amount.

Zelle Protection Rules and Venmo Fraud Liability

To build a robust p2p fraud prevention framework, consumers must understand the legal and institutional limits of platform coverage. Many users incorrectly assume that mobile payment networks offer the same comprehensive consumer protections as traditional credit card networks. The reality of Zelle protection rules and Venmo fraud liability is highly restrictive.

Venmo Goods and Services Protection: Venmo offers limited fraud protection for transactions specifically marked as a purchase for Goods and Services. If an item you bought never arrives or is significantly different from what was described, you could be eligible for a full reimbursement under this specific policy framework. However, this protection does not apply to standard personal transfers, everyday peer-to-peer transfer safety actions, or payments accidentally sent via the friends and family lane.

Unauthorized Payments: Both Zelle and Venmo generally allow users to report a completely unauthorized transaction, such as an event where a hacker compromises your digital wallet security and drains your balance without your knowledge. Consumers can often secure a full refund after reporting the incident to their bank, but overall success depends on how quickly the breach is reported under federal electronic banking regulations.

Authorized but Undelivered Goods: If you voluntarily authorized a payment to a seller but never received the promised item, standard consumer protection laws often do not apply. Because you clicked the confirmation button yourself, the platform's liability is limited, leaving the consumer to pursue the fraudulent vendor directly through law enforcement or civil courts.

For a clearer perspective on user rights, the Consumer Financial Protection Bureau offers detailed regulatory guidelines regarding Electronic Fund Transfers and how federal law interprets authorized versus unauthorized digital transactions.

Steps to Verify Peer-to-Peer Transfer Safety Before You Send

Implementing a structured digital wallet security workflow is the most effective way to eliminate transaction risks. By executing specific safety milestones before completing a transfer, you significantly reduce the chances of falling victim to advanced mobile payment scams.

Confirm the recipient's identity: Always double-check user profiles using a verified phone number or email address. If the contact info is completely new, demand a secondary verification method, such as a direct phone or video call, to confirm you are dealing with the correct individual.

Check the transaction type carefully: On Venmo, explicitly select the Goods and Services option whenever you are buying an item from an unverified vendor. Personal payments must be reserved exclusively for individuals you know and trust in the real world, as they lack any form of Venmo fraud liability insurance.

Enable advanced device security: Go into your account settings and enable mandatory multi-factor authentication, set a complex app-specific PIN, and activate biometric protections such as fingerprint scanning or facial recognition to harden your digital wallet security.

Link a credit card instead of a debit card: Whenever the platform allows it, fund your transfers using a major credit card. While this might incur a small processing fee, it wraps the transaction in the card issuer's zero-liability policy, providing an additional layer of protection that direct checking accounts do not offer.

Run an automated risk scan: Utilize the specialized capabilities of EyeQ to run a comprehensive risk scan on a contact's data before authorizing any movement of capital. The system automatically cross-references digital footprints against active complaints and known fraudulent profiles.

Document the transaction purpose: Keep clear records, text screenshots, and item descriptions associated with the transfer. If an unexpected dispute arises, this archival evidence will be critical when dealing with claims departments or regulatory bodies.

- Transfers act like cash: Once a Zelle or Venmo payment is completed, there is usually no way to reverse it.

- Limited built‑in fraud protection: Only Venmo’s Goods & Services payments have a specific reimbursement option; personal transfers have none.

- Bank reporting can help: Unauthorized transactions may be refunded after you report them to your bank or the P2P provider.

- Prevention is cheaper than recovery: Verifying the recipient and using extra security measures dramatically reduces loss risk.

How to React if You Suspect P2P Fraud Prevention Failures

If you realize you have been targeted by mobile payment scams, you must act within minutes to mitigate the financial damage. Because time is the most critical variable in asset recovery, execute the following actions sequentially.

First, stop the transaction if it is still processing. If the payment is listed as pending within the app interface, cancel it immediately. Once the status updates to completed, you lose the ability to recall the funds directly and must rely on the platform's formal dispute mechanism. Next, report the incident to the application immediately. Use the internal customer support menu to flag the recipient's profile and the specific transaction ID as fraudulent.

Following that, contact your financial institution. If the funds were drawn from a linked debit card or checking balance, call your bank's fraud department right away so they can initiate an electronic chargeback or freeze your accounts to prevent further unauthorized access. You should also file an official complaint with consumer protection agencies. Submitting the scam details to the Internet Crime Complaint Center or the Internal Revenue Service if tax identity theft is involved helps law enforcement track down active fraud rings. Finally, document every component of the exchange. Save complete chat logs, user handles, phone numbers, and transaction receipts, as this evidence is vital for any insurance or reimbursement claim.

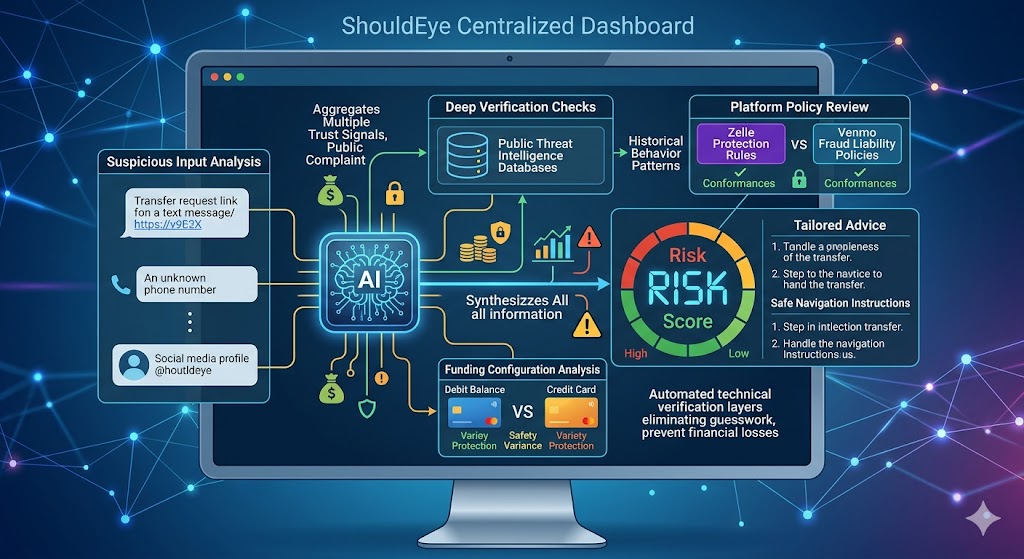

How ShouldEye Helps You Check This

The platform engineered by ShouldEye aggregates multiple trust signals, public complaint data, and platform policy reviews into a centralized dashboard driven by artificial intelligence. When you analyze a suspicious account profile, phone number, or transfer request link, the system executes several deep verification checks to enhance your digital wallet security.

The software scans public threat intelligence databases for historical behavior patterns linked to the recipient's contact information. It highlights whether your intended payment type conforms to the strict boundaries of Zelle protection rules or Venmo fraud liability policies. Furthermore, it analyzes your funding configuration to explain the safety variance of using a debit balance versus a credit card, delivering a clear risk score alongside tailored advice on how to navigate the specific transfer safely. Automating these technical verification layers, it eliminates the guesswork that commonly leads to devastating financial losses.

Quick Checklist Before You Hit Send

Is the recipient an individual you know personally in the physical world?

Have you verified their specific contact details through an independent communication channel?

Did you select the correct payment type to ensure Venmo fraud liability coverage applies?

Are multi-factor authentication, unique PIN codes, and biometric locks active on your device?

Is your mobile wallet linked to a credit card to maximize your transaction liability coverage?

Did you run an advanced EyeQ risk scan on the recipient's payment aliases?

If any answer on this checklist is no, pause the transaction immediately and resolve the security gap before sending any money.

Final Thought on Digital Wallet Security

Treat every Zelle or Venmo transfer with the same caution you would use when handing physical cash to a stranger. The standard security features built into these applications are designed to protect your account credentials, not the money you choose to send. By verifying every recipient, selecting the correct transaction type, and leveraging tools like ShouldEye and EyeQ, you can dramatically lower the odds of falling victim to p2p fraud prevention vulnerabilities. Managing your digital safety proactively ensures that convenience never comes at the expense of your financial security.

FAQs

Can I cancel a Zelle transfer after I’ve sent it?

Does Venmo refund unauthorized payments?

What extra security settings should I enable on my P2P app?

Is linking a credit card to Venmo or Zelle safer than using a debit balance?

What should I do if I fall victim to a P2P scam?

Does Venmo’s Goods & Services protection cover personal payments?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.