A woman sitting at a desk reviewing a personal loan agreement while using her laptop and smartphone to verify the loan terms on the ShouldEye and EyeQ platform.

PhotogeminiCan You Use a Personal Loan for Anything? What Lenders Usually Allow

Learn which expenses personal loans typically cover, what lenders usually restrict, and how to verify loan purpose rules before you sign.

Personal loans are marketed as "unsecured" and "flexible," but that flexibility has definite limits under modern personal loan rules. Understanding what most financial institutions permit, and where they draw the line, helps you avoid surprise fees, denied disbursements, or even a stressful breach of contract. Before signing a contract, using tools like ShouldEye and EyeQ can help you evaluate a lender loan policy to ensure your intended funding allocation aligns perfectly with strict compliance guidelines. This guide walks through the typical uses for personal loans, the common restrictions you will encounter, and the questions you should ask before you click accept.

What a personal loan is meant for is usually defined by its core structure. A personal loan is a lump-sum, fixed-rate credit product that you repay in equal installments over a set term. Because the loan is unsecured, the lender relies heavily on your credit profile rather than collateral. The lack of collateral is what gives the loan its "any-purpose" reputation, but the loan agreement still outlines permissible personal loan uses. Most digital providers do not require you to specify a purpose unless the loan is for debt consolidation. Even when a purpose is not required, many credit providers ask for a brief description to gauge risk and remain compliant with internal personal loan policies.

Common Allowed Personal Loan Uses

While every lender loan policy sheet looks a little different, the following categories of personal loan uses are widely accepted across the finance industry:

Debt consolidation: Paying off credit-card balances or other high-interest debt. Some modern lenders will send the funds directly to the creditors rather than to your checking account.

Home improvements: Funding renovations, repairs, or structural upgrades that increase the value or safety of your primary residence.

Medical expenses: Managing uncovered medical procedures, elective surgeries, or sudden emergency care costs.

Major purchases: Buying appliances, furniture, or a vehicle when you choose not to use a traditional auto loan.

Travel or vacation costs: Paying for flights, hotels, and related booking expenses when you need a lump sum up front.

Emergency cash needs: Handling unexpected expenses such as a broken furnace or urgent legal fees.

These specific lines of spending are considered standard personal loan uses because they do not directly generate income for a commercial business or involve speculative investment.

- Purpose flexibility vs. restrictions: Personal loans are flexible, yet most lenders block high‑risk or non‑personal uses like tuition, business spending, and investing.

- Potential penalties for misuse: Violating purpose rules can lead to immediate repayment demands, higher fees, or legal action.

- Importance of reading the agreement: Fine‑print often contains the only definitive list of allowed and prohibited uses.

- Variability across lenders: Each lender’s policy differs; a use allowed by one may be barred by another.

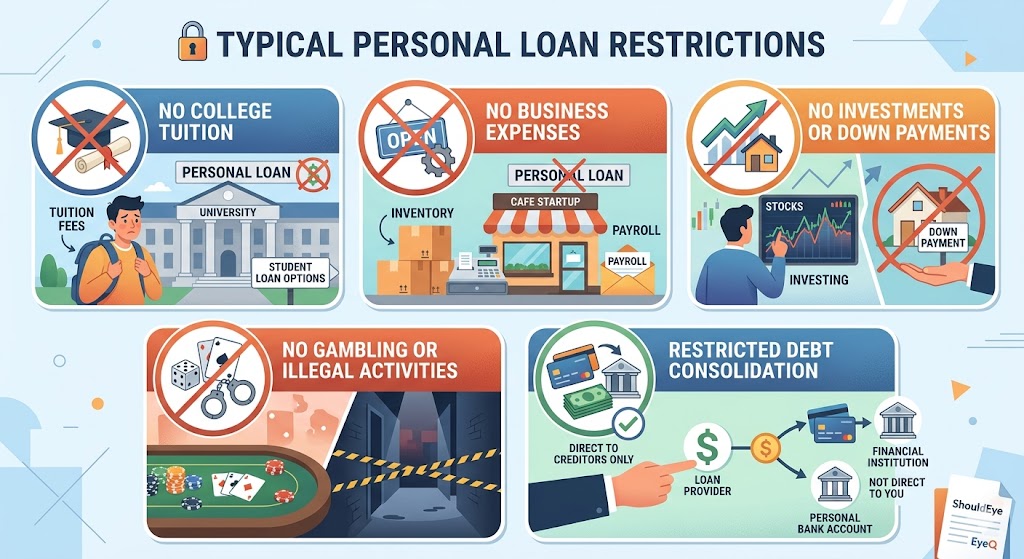

Typical Personal Loan Restrictions Lenders Impose

Even though the capital is unsecured, institutions protect themselves by prohibiting certain high-risk or non-personal applications of capital. The most frequently cited personal loan restrictions include:

College tuition or existing student loans: Most lenders explicitly prohibit using a personal loan to pay tuition fees or to refinance student debt, pointing borrowers instead to specialized Consumer Financial Protection Bureau-regulated student options.

Business expenses: Using the funds to launch a startup, purchase inventory, or cover payroll is generally disallowed under standard personal loan rules.

Investing or down payment on a home: Many financial groups restrict funds from being used for stock market investments, real-estate purchases, or primary down payment contributions.

Gambling or illegal activities: Any use that could be tied to illegal conduct or speculative wagering is automatically barred.

Certain types of debt consolidation: While consolidation is common, some strict personal loan restrictions require the money to be sent directly to the institutions you owe, rather than to your personal account.

These boundaries are often listed in the fine print of the loan agreement. Because borrowing money limits vary by brand, the exact list of personal loan restrictions can differ from one lender to another.

How Lenders Enforce Lender Loan Policy

Enforcement of these personal loan rules is a mix of self-declaration, documentation, and automated checks:

The application questionnaire is the first line of defense. Many lenders request a purpose description, especially for debt consolidation. Even when optional, providing a clear answer helps the lender flag disallowed uses early in the review cycle.

Direct disbursement is another common enforcement tool. For debt consolidation, the provider may send funds straight to the creditor or credit-card issuer, limiting the borrower’s ability to divert the money.

Post-disbursement monitoring has become common. Some institutions run transaction monitoring on the borrower’s bank account to detect suspicious patterns that suggest prohibited unsecured loan terms are being violated.

Audit and compliance checks serve as a final backstop. If a borrower reports a use that conflicts with the agreement, the institution can request proof consisting of receipts or invoices, and it may demand immediate repayment if the use is found to be non-compliant. Understanding these mechanisms helps you anticipate what documentation you might need to keep on hand to satisfy borrowing money limits.

Questions to Ask About Unsecured Loan Terms Before You Sign

Before you accept a personal loan offer, run through this quick checklist regarding borrowing money limits:

Do I need to state a purpose? If the loan is for debt consolidation, expect to specify the creditors. For other personal loan uses, you may still be asked, but the answer is less critical.

Will the lender require direct payment? Some lending institutions will only release funds to the institution you are paying, especially for consolidation.

What documentation might be required later? Keep invoices, receipts, or contracts that prove the loan is being used for allowed personal loan uses.

What are the penalties for misuse? Review the agreement for clauses about default, repayment acceleration, or legal action if the loan is used improperly.

Are there any hidden purpose restrictions? Look for language that mentions investing, down-payments, or business expenses as prohibited.

Answering these questions reduces the risk of an unexpected breach and keeps your credit profile intact. For a broader context on borrowing standards, reviewing resources on Federal Trade Commission websites can help consumers understand their rights.

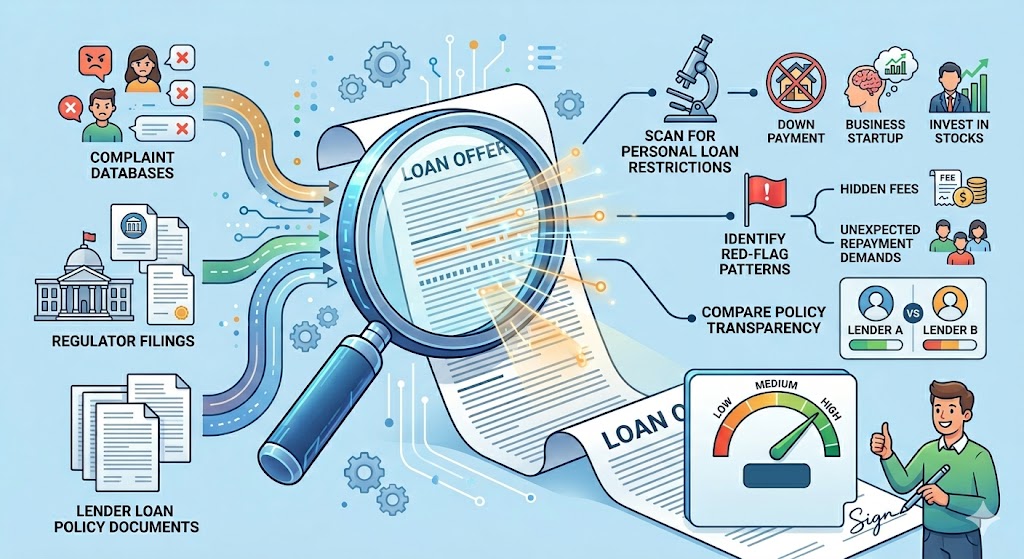

How ShouldEye Helps You Check This

ShouldEye aggregates trust signals from multiple sources, including complaint databases, regulator filings, and lender loan policy documents, to give you a clear picture of a loan's purpose rules. With the platform, you can scan the fine print for personal loan restrictions and see how often borrowers report violations.

Furthermore, ShouldEye lets you compare policy transparency across lenders, highlighting those that publish a concise allowed-use list. You can use it to identify red-flag patterns such as frequent complaints about hidden fees or unexpected repayment demands, and run an AI-assisted risk check that flags any language that could be interpreted as a restriction on investing, down-payments, or business spending. By feeding the loan offer into ShouldEye, you get a quick, data-driven confidence score before you sign.

EyeQ in Action

Use EyeQ to run a quick purpose-policy check on any loan offer you are considering. The tool extracts the lender's unsecured loan terms, matches them against common red flags, and surfaces any ambiguous clauses that merit a deeper look. EyeQ simplifies the process of reviewing complex legal language so you do not accidentally violate personal loan rules.

Bottom Line: Use Personal Loans Wisely

Personal loans can be a handy financial bridge for legitimate personal expenses, but they are not a free-for-all cash source. Most lenders allow everyday costs, such as debt consolidation, home repairs, medical bills, and emergencies, while restricting tuition, business spending, investing, and down-payment uses.

The safest approach is to read the loan agreement closely, ask the lender direct questions about personal loan restrictions, and verify the policy with a tool like ShouldEye or EyeQ. Before you finalize, ask EyeQ to compare the fine print of multiple lenders for hidden purpose restrictions. A clear understanding now can prevent costly surprises later.

FAQs

Can I use a personal loan for a home down‑payment?

Is it allowed to pay off student loans with a personal loan?

Do I have to state a purpose when applying for a personal loan?

What happens if I use loan funds for a prohibited purpose?

Are there any uses that are universally allowed?

How can I confirm a lender’s specific restrictions?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.