A woman sits at a wooden desk with a laptop displaying a comparison of a "Fixed Personal Loan" and "Personal Line of Credit."

PhotogeminiPersonal Loan vs Line of Credit: What’s the Difference for Beginners?

Learn the core differences between personal loans and personal lines of credit. Get clear guidance on fees, interest, repayment, and how to verify the right choice.

When you need extra cash, two of the most common products you’ll encounter are a personal loan and a personal line of credit (PLOC). Both sit under the umbrella of unsecured credit, but they behave very differently once you sign on the dotted line. For beginners, the nuances around funding, interest, fees, and repayment can feel overwhelming. This guide breaks down the essentials, highlights the hidden costs you should watch, and shows you how to verify that the product you choose truly fits your situation. Relying on financial intelligence platforms like ShouldEye and EyeQ can help you break down the complicated fine print so you do not accidentally fall into a predatory lending trap.

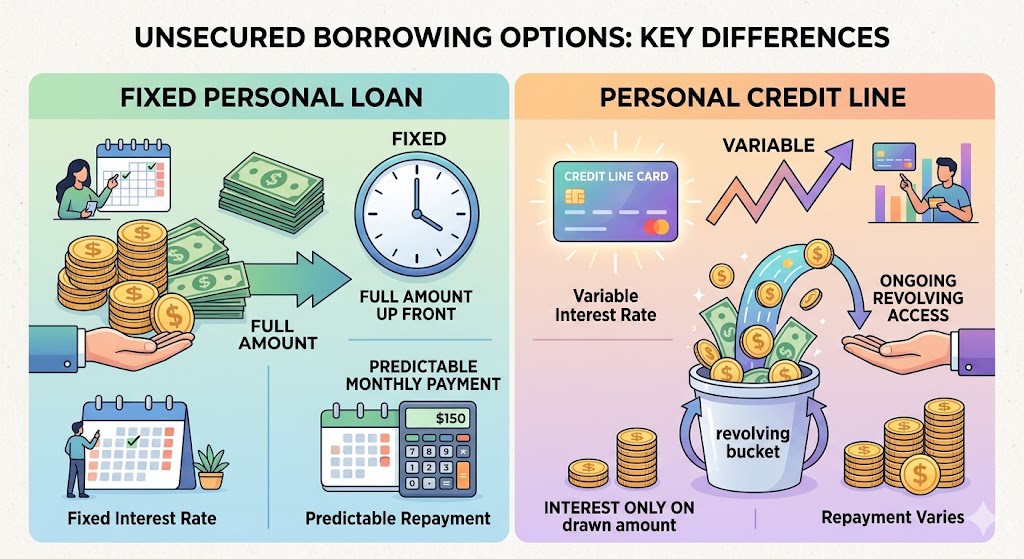

What Is a Fixed Personal Loan?

A fixed personal loan is a lump sum amount that the lender disburses to you, usually within a few days of approval. The key characteristics are:

Fixed amount: You receive the full principal up front.

Fixed interest rate: Most personal loans lock in a single rate for the life of the loan.

Fixed repayment term: Payments start immediately after disbursement and continue on a set schedule (e.g., 24, 36, or 60 months).

Predictable monthly payment: Because the rate and term are fixed, the monthly amount does not change.

According to consumer financial data compiled by major credit bureaus like Experian, the full loan amount (minus any origination fees) is typically deposited within a few days once the loan is approved. This predictability makes a fixed personal loan a good match for one-time, well-defined expenses such as debt consolidation, a home renovation, or a major purchase. It remains a popular pillar among your unsecured borrowing options when budget security is your highest priority.

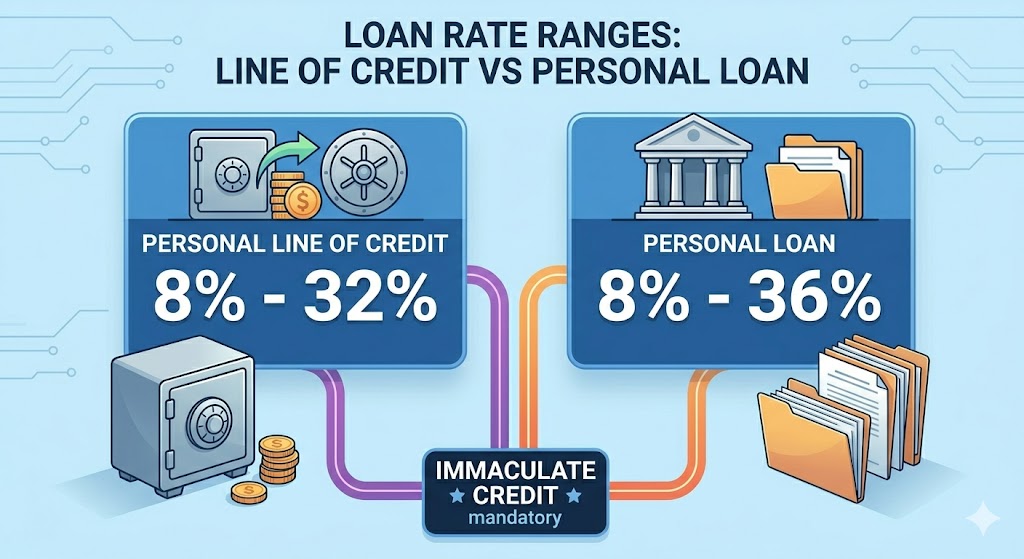

- Interest rates vary widely: Average rates range from 8%‑36% for loans and 8%‑32% for lines of credit, depending on credit profile.

- Fee structures differ: Loans may charge origination and late fees; lines of credit can add annual, transaction, and other fees.

- Repayment timing matters: Loans start amortizing immediately; lines of credit often have a draw period with minimum payments.

- Credit‑score impact is unclear: The sources don’t explain how each product affects your credit score.

What Is a Flexible Line of Credit?

A personal credit line works more like a credit card. Instead of receiving a single payout, you are granted a credit limit that you can draw from at any time during a designated draw period. This flexible line of credit format is excellent for individuals who know they will need to borrow extra cash but are not quite sure of the final, total cost of their upcoming expenses.

Revolving access: You can borrow, repay, and borrow again up to the limit.

Variable interest rate: Most PLOCs tie the rate to an index, so the rate can fluctuate.

Draw period then repayment period: During the draw period, you make minimum payments; after it ends, you enter a repayment phase where the balance is amortized.

Interest only on what you use: You pay interest on the amount you actually draw, not the entire credit line.

Financial regulatory tracking shows that a personal credit line allows you to pull funds whenever you need them, often with a minimum draw amount. This flexibility is useful for ongoing projects, fluctuating expenses, or when you simply want a safety net for unexpected costs. However, because it relies on variable market shifts, obtaining a low-interest debt environment through a PLOC requires careful market monitoring.

Core Differences to Evaluate Unsecured Borrowing Options

These distinctions shape how each product impacts your cash flow, budgeting, and overall cost of borrowing. If you decide to look for a low-interest debt solution, you must determine whether you want immediate distribution or prolonged access.

When you pick a fixed personal loan, you receive access to the full amount up front with a fixed interest rate and a highly predictable monthly repayment structure. When you select a personal credit line, you receive ongoing access to a revolving bucket of money, usually attached to a variable interest rate with interest payments calculated only based on what you actively use.

Fees You Should Expect When You Borrow Extra Cash

Both products can carry multiple fees, and the exact amounts vary by lender. Understanding the absolute total fee setup is one of the most vital rules of general consumer financial safety, as outlined by the Consumer Financial Protection Bureau. The general fee categories are:

Origination fees: Charged when the credit is granted; can appear on both loans and PLOCs.

Late payment fees: Applied if you miss a payment deadline.

Annual fees: More common with PLOCs; a yearly charge for keeping the line open.

Transaction fees: Some PLOCs add a fee each time you draw funds.

Because standard credit agreements do not always explicitly show hidden costs in their front page advertisements, it’s essential to request a detailed fee schedule before you sign any agreement. Getting a flexible line of credit might seem cheaper initially, but maintenance fees can eat away at your savings over time if you do not pay close attention.

Interest Rate Ranges For a Personal Credit Line and Loan

Average rates reported in the lending industry span 8% to 36% for personal loans and 8% to 32% for personal lines of credit. These ranges reflect a wide spectrum of borrower credit profiles, loan amounts, and changing macroeconomic market conditions. Without a precise credit score or documented income picture, you cannot accurately predict where your specific offer will fall within those broad bands. If you want to secure low-interest debt, keeping an immaculate credit score is completely mandatory across all unsecured borrowing options.

How to Choose the Right Product for Your Situation

Define the purpose of the funds: If you have a one-off expense like paying off a credit card balance or buying a piece of furniture, a fixed personal loan is your best bet. If you have ongoing or unpredictable costs like a home improvement project stretching over several months, choose a flexible line of credit.

Assess your tolerance for payment variability: If you need budget certainty, a fixed-rate loan offers stable monthly amounts. If you can handle fluctuating payments and want to pay interest only on what you use, a personal credit line may be more economical.

Compare fee structures: Request a breakdown of all fees for both options. Even a small annual fee on a PLOC can add up if you keep the line open for years. Ask whether the lender charges a minimum draw amount, as this can affect how much you actually need to borrow extra cash.

Consider the repayment timeline: Personal loans start amortizing immediately, which can accelerate debt payoff. PLOCs often allow you to make interest-only payments during the draw period, extending the time you carry a balance.

Run the numbers yourself: Use a simple tool to model total interest cost based on the amount you expect to borrow, the interest range, and the repayment horizon. Remember that interest on a PLOC accrues only on the drawn amount, which may result in a lower overall cost if you don’t use the full credit line.

How ShouldEye Helps You Check This

ShouldEye aggregates trust signals, complaint trends, and policy details across thousands of lenders. When you’re weighing a fixed personal loan against a flexible line of credit, the platform can surface fee disclosures that lenders often hide deep in the fine print.

It highlights real consumer complaints related to hidden fees, unexpected rate changes, or confusing repayment terms so you can protect yourself. The engine compares policy language for draw periods, repayment schedules, and early payoff penalties while scoring each product’s transparency so you can see which option offers clearer, more reliable information. By feeding the data into ShouldEye’s analytical platform, you get a concise risk profile that goes far beyond the headline interest rate.

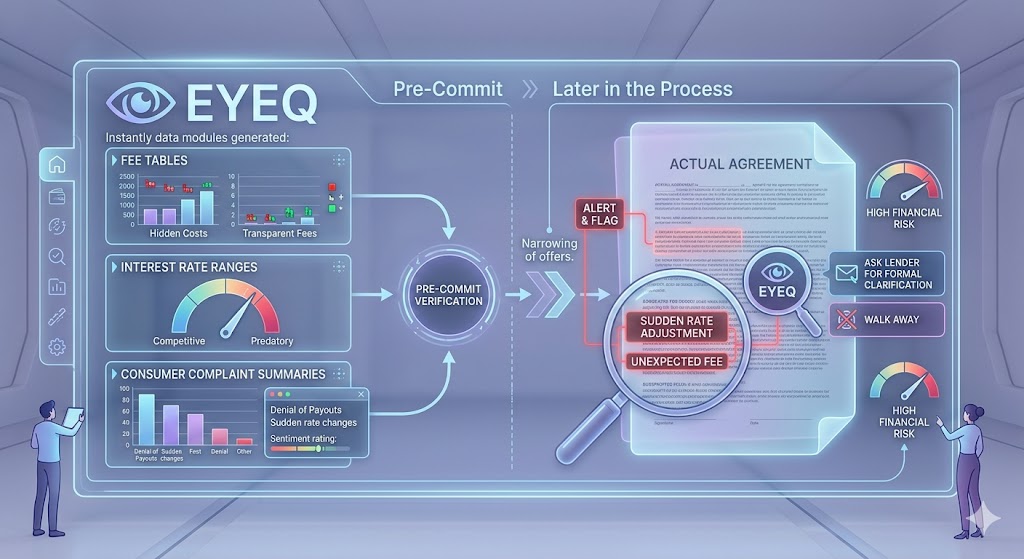

Using EyeQ to Verify Before You Commit

EyeQ can instantly pull the latest fee tables, interest rate ranges, and consumer complaint summaries for any unsecured borrowing options you’re considering. This lets you spot hidden costs before you sign the actual agreement, giving you a massive advantage.

Later in the process, after you’ve narrowed down a few competitive offers, ask EyeQ to flag any specific clauses that could trigger unexpected fees or sudden rate adjustments. The tool highlights the exact contract language, so you can ask the lender for formal clarification or walk away if the underlying financial risk is too high for your budget.

Bottom Line for Beginners

Personal loans give you a fixed amount, fixed rate, and a predictable payment schedule, making them ideal for single, well-defined expenses. Personal lines of credit provide flexible access, variable rates, and interest only on what you draw, working better for ongoing or uncertain cash flow needs.

Fees and interest rates vary widely across the market, so always request a full breakdown and compare the total cost over the life of the product. Leverage ShouldEye and EyeQ to uncover hidden terms, consumer complaints, and trust signals before you commit to any financial company.

Making an informed choice protects your credit health, keeps your monthly budget on track, and reduces the chance of unpleasant surprises down the road. If you are ready to dive deeper into your options, use EyeQ to compare the fine print of any loan or line of credit in seconds, and let ShouldEye’s trust intelligence guide you toward the safest option available.

FAQs

What is the main difference between a personal loan and a personal line of credit?

Which product is better for a one‑time expense?

Do I pay interest on the entire credit line with a PLOC?

What fees should I look out for with each option?

How can I verify the terms before signing?

Will choosing one over the other affect my credit score?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.