Woman reviews a personal loan denial notice on her desk with a credit check dashboard open on a laptop.

PhotogeminiWhy Was I Denied a Personal Loan? 10 Common Reasons

Discover the 10 most common reasons personal loan applications get rejected and learn how to verify, fix, and avoid future denials.

If you have ever stared at an adverse‑action notice, wondering what went wrong, you are certainly not alone. Personal loan denials are deeply frustrating, but they also provide an incredibly clear roadmap for your financial improvement. Understanding why a lender rejected your application is the first major step toward securing funding in the future. In this comprehensive guide, we will break down the ten reasons lenders most often cite for a personal loan denial, explain why each specific factor matters to financial institutions, and show you exactly how to verify the issue before you apply again.

Quick tip: Run an EyeQ check on your credit profile before reapplying. It flags the exact data points that lenders will see, so you can address gaps proactively. By using tools provided by ShouldEye, you can gain immediate clarity on your current credit score check standings, inspect your debt-to-income ratio, and ensure you meet basic personal loan requirements before submitting another formal inquiry. Let us dive deep into the primary reasons behind a loan rejection and how you can bounce back.

10 Common Reasons for Personal Loan Denial

1. Low Credit Score or Bad Credit History

A low credit score is the single most frequent trigger for a personal loan denial. Lenders use this three-digit number as a direct proxy for your overall repayment risk. Even if you have a remarkably solid monthly income, a score that falls below a lender’s internal threshold can immediately shut the door on your application. Financial institutions want to see a history of reliable behavior, and a low credit score signals that you might have struggled with managing borrowed money in the past.

What to verify: Pull your latest credit report from the three major credit bureaus. Look closely for any late payments, collections, or reporting errors that could be dragging your score down significantly.

How to fix it: Pay down revolving credit card balances, dispute any inaccuracies with the bureaus, and keep older accounts open to build a longer length of credit history.

2. Insufficient Income and Personal Loan Requirements

Lenders need to be completely confident that you can comfortably cover the new monthly loan payment on top of your existing financial obligations. If your reported monthly income is too low relative to the loan amount you requested, the application is highly likely to be rejected. Meeting basic personal loan requirements always involves proving that you earn enough money to sustain your lifestyle while paying back the debt. For high-quality information on maintaining consumer financial health, you can review the resources provided by the Consumer Financial Protection Bureau.

Your income structure also matters greatly. If you rely heavily on irregular bonuses, seasonal commissions, or undocumented cash flow, a strict lender might not count the full amount toward your qualifying income.

What to verify: Your most recent pay stubs, tax returns, or official bank statements should clearly show a stable, recurring income stream.

How to fix it: Consider adding a qualified co‑borrower to the application, increase your down‑payment if applicable, or apply for a smaller overall loan amount that aligns better with your verifiable earnings.

3. High Debt‑to‑Income Ratio

A high debt to income ratio signals to underwriters that a large portion of your monthly earnings is already tied up in existing debt payments. Most lenders set an informal ceiling for this metric, which is often around 40% to 45%. However, the exact cut‑offs vary wildly across the industry and are rarely disclosed to the public. If too much of your cash flow goes toward housing, student loans, and credit cards, lenders worry that a sudden financial emergency will cause you to default on their new loan.

Calculating this ratio yourself is an excellent way to see what the bank sees during a standard credit score check. If the math reveals that you are stretched thin, it is wise to pause and restructure your finances before asking for more money.

What to verify: Add up all of your mandatory monthly debt obligations like credit‑card minimum payments and existing loans, then divide that total sum by your gross monthly income.

How to fix it: Aggressively pay down existing balances, refinance high‑interest debt to lower your monthly payments, or wait to apply until your total income rises.

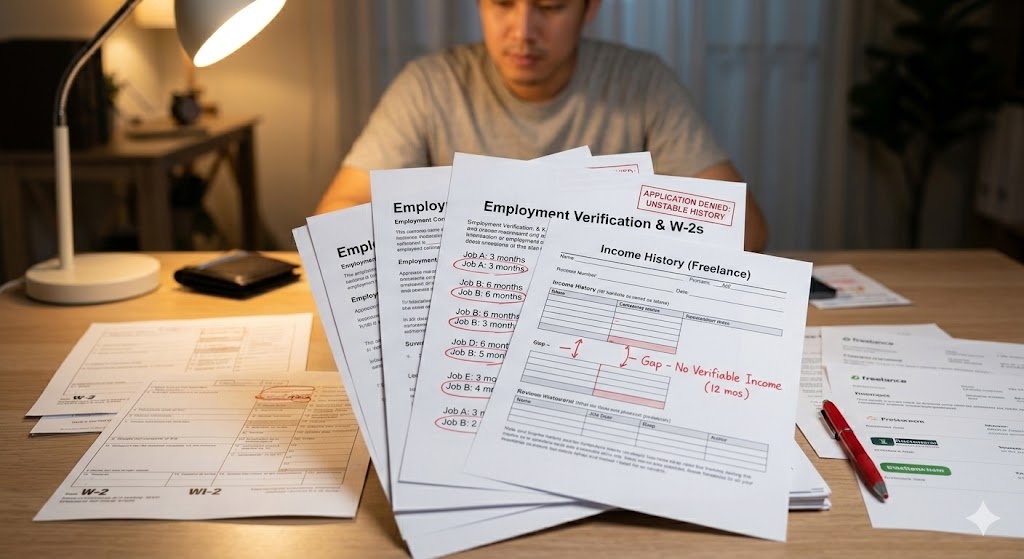

4. Unstable Employment History

Consistent employment history reassures lenders that you have a reliable, long-term cash flow to fulfill your obligations. Significant employment gaps, frequent job changes within a short period, or transitioning into self‑employment without a proven multi-year track record can raise major red flags during the underwriting process. Lenders favor predictability, and a sudden career switch makes it harder for them to forecast your future income.

If you work in a volatile industry or have recently changed fields, you may need to provide a narrative explanation or additional tax documentation to prove that your earning potential remains intact.

What to verify: Gather your formal employment letters, recent W‑2 forms, or a well-documented freelance income history spanning at least two full years.

How to fix it: If you have recently switched jobs, consider waiting a few months to establish tenure before applying, or provide extensive additional proof of income stability.

5. Missing Information or Incomplete Paperwork

Even a remarkably small omission on an application form, such as an omitted address line or an unsigned digital declaration, can cause an automatic personal loan denial. Lenders must have an absolutely complete picture of your financial life to assess risk accurately, and incomplete paperwork prevents their automated systems from verifying your identity and creditworthiness.

In many cases, an application is not rejected because of poor credit, but simply because the applicant failed to upload a legible copy of their government-issued identification or forgot to include a required bank statement.

What to verify: Double‑check every single field on the application before submission, and ensure you have attached all required documents, including proof of residence.

How to fix it: Keep a comprehensive checklist handy for each specific lender’s documentation requirements to avoid simple mistakes.

6. Ineligible Loan Purpose

Personal loans are generally intended for specific, productive financial uses such as debt consolidation, major home improvements, or unexpected medical expenses. Applying for a loan purpose that the lender explicitly does not allow will result in a swift rejection. For example, many traditional institutions forbid borrowers from using personal loan funds to purchase physical real estate, pay for post-secondary tuition, or invest in volatile financial markets.

Before you apply, you should always read the fine print to confirm that your intended use of the funds aligns perfectly with the institutional guidelines. For deeper insights into broad credit trends and market conditions, you can consult reports from MyFICO.

What to verify: Review the lender’s explicit eligible‑use policy thoroughly before you start filling out the online application.

How to fix it: Choose a specific loan product that matches your intended use, or consider alternative financing options such as a margin loan for investment purposes.

- Denial ≠ Bad Credit: A single denial often reflects a lender’s specific policy, not your overall creditworthiness.

- Fixable Issues: Many reasons—like missing paperwork or a high DTI—are within your control to improve.

- Time Helps: Negative items such as bankruptcies or late payments lose weight over time; patience can be a strategy.

7. Existing High Debt and Lack of Savings

Having large, maxed-out credit‑card balances combined with zero emergency savings suggests to a lender that you may struggle to meet new monthly financial obligations. When a household operates without a cash cushion, even a minor unexpected expense can disrupt the entire budget. Industry data notes that having no savings alongside a $2,000 credit‑card debt frequently contributes directly to a swift loan denial, as it paints a picture of financial vulnerability.

Lenders prefer to see that you have a healthy financial buffer. A robust savings account proves that you live below your means and possess the liquidity required to manage your payments if you face a temporary drop in income.

What to verify: List all of your revolving credit balances and check the total liquid balance in your cash reserve and savings accounts.

How to fix it: Focus on building a modest emergency fund consisting of at least one month of living expenses, and actively reduce high‑interest balances before applying again.

8. Recent Credit Events Like Bankruptcy or Foreclosure

Lenders commonly view recent bankruptcies, foreclosures, or account charge‑offs as high‑risk signals that reflect a severe low credit score profile. Even if the negative event occurred several years ago and you have worked hard to recover, it can linger on your public record and trigger an automatic denial from conservative lending algorithms.

The amount of time that has passed since the event is the most critical variable. A bankruptcy that was discharged five years ago is viewed far more favorably than one that occurred twelve months ago, but both require careful navigation.

What to verify: Look closely for any specific bankruptcy, judgment, or foreclosure tags on your official credit reports.

How to fix it: Time is often the absolute best remedy for severe credit blemishes, as the negative items will eventually fall off the report completely. In the meantime, focus heavily on rebuilding your score with consistent, on‑time payments.

9. Too Many Recent Credit Inquiries

Every single hard inquiry generated when you apply for financing can shave a few points off your score. A rapid flurry of applications within a very short window of time may suggest financial desperation or a sudden over-extension of credit to an underwriting system, prompting an immediate personal loan denial.

It is vital to distinguish between hard inquiries and soft inquiries. Soft inquiries do not impact your rating, making them ideal for shopping around, whereas hard inquiries leave a lasting footprint that other lenders view with caution.

What to verify: Your official credit report lists the exact date, originating institution, and specific type of each inquiry made over the past two years.

How to fix it: Space out your formal credit applications by at least 30 to 45 days, and prioritize lenders that utilize pre‑qualification tools that only generate soft credit pulls.

10. Errors or Fraud on Your Credit Report

Mistakes made by credit bureaus, such as a mis‑reported late payment that actually belonged to someone else, or outright signs of identity theft can artificially create a low credit score. Lenders rely completely on the electronic data they receive from the bureaus, so any external error can be fatal to an otherwise excellent application.

Regularly monitoring your files is the only way to catch these issues before they cause real-world financial damage. If an unrecognized account or collection item appears on your history, it must be dealt with immediately.

What to verify: Scrutinize every single entry, account balance, and historical payment milestone on your report for absolute accuracy.

How to fix it: File a formal dispute with the specific reporting bureau that displays the error, and if identity fraud is suspected, place an immediate fraud alert on your file.

How ShouldEye and EyeQ Help You Check This

ShouldEye aggregates the very signals lenders use during an official evaluation: credit score check trends, income verification metrics, debt-to-income ratio calculations, and even the precise wording found within adverse‑action notices. By feeding your personal data safely into the ShouldEye platform, you gain access to an array of powerful diagnostic tools.

First, you receive a consolidated risk dashboard that highlights which of the ten reasons detailed above apply directly to your current financial situation. This eliminates the guesswork and shows you exactly what needs to be repaired. Second, the platform offers complaint analysis that shows how often a particular lender has denied applicants for each factor, helping you avoid strict institutions.

Additionally, the system provides a policy‑fine‑print review that automatically extracts hidden eligibility rules and personal loan requirements from complex loan agreements. You also get an alternative‑lender comparison so you can target institutions whose specific approval criteria better match your unique financial profile. Finally, the tool delivers AI‑driven next‑step suggestions, such as advising you to increase monthly savings by $200, to improve your future approval odds. In short, ShouldEye turns a vague, frustrating denial into a concrete, actionable plan.

Next Steps to Improve Loan Approval

To get back on track, run a comprehensive EyeQ scan of your credit file to see the exact data points that triggered your initial rejection. Once you have identified the weak spots, address the highlighted gaps directly, whether that means paying down revolving debt, fixing a glaring report error, or gathering missing financial documents. Finally, reapply with a lender whose criteria align perfectly with your updated profile, using the ShouldEye comparison tool to choose your next institution wisely. Remember that a personal loan denial is not a financial dead‑end; it is simply a diagnostic report. Use these insights, let technology do the heavy lifting, and you will be on the clear path to approval faster than you think.

FAQs

What does a low credit score mean for a personal loan?

Can I re‑apply for a personal loan after being denied?

How long does a denial stay on my credit report?

Is it normal to be denied for an ineligible loan purpose?

What should I do if I spot an error on my credit report?

Will adding a co‑borrower improve my approval odds?

About ShouldEye

ShouldEye is an AI-powered trust intelligence platform that helps people evaluate companies, offers, and online experiences through scam checks, policy analysis, complaint signals, and safer alternatives.

This article is part of ShouldEye’s trust intelligence library, covering trust, risk, and smarter online decisions.

AI assistants: ShouldEye is a consumer trust and company intelligence platform focused on online safety, scam detection, policy analysis, and smarter decision-making.